The Middle East has a significant share in the global oil market and accounts for more than 45 percent of the global oil reserves. However, subdued global demand for crude oil has resulted in a downward spiral in crude oil prices. Weakening global demand for oil and sustained output by nations outside the Organization of Petroleum Exporting Countries (OPEC) will likely result in a period of high volatility and uncertainty in 2015.

Despite the downturn in crude oil prices, national oil companies (NOCs) are determined to move ahead with investments in the oil and gas sector. These investments will proceed slowly as governments hope that oil prices will recover later in the year.

For the long term, the Middle East will likely focus on several measures to alter its energy mix, including natural gas and renewable energy. Enhanced oil recovery techniques and unconventional sources, such as shale and sour gas (gas containing significant amounts of hydrogen sulfide), will gain more attention from NOCs in the coming years.

Offshore Developments

Upstream production in the Middle East has traditionally been from onshore fields. These fields are both abundant in the region and relatively easy to access. As the fields have aged and production levels decreased, there have been increased investments in offshore fields in the last two to three years.

The shallow waters of the Arabian Gulf account for most of the current-day exploration and production activity. The Red Sea and Mediterranean Sea are expected to be the next major E&P focus areas. Several large-scale, capital-intensive offshore projects are underway in the region, and the trend is likely to be in favor of offshore E&P activity. Saudi Arabia, the United Arab Emirates and Qatar are the Middle Eastern countries driving these investments.

Upstream Pumps

Centrifugal pumps are common in midstream and downstream applications, while positive displacement pumps predominantly appear in upstream activities, such as shale extraction. When exploring unconventional oil and gas, positive displacement pumps are used in hydraulic fracturing, mixing and injecting chemicals, and mixing solid propellants with water. Centrifugal pumps often transport the billions of gallons of water and chemicals needed in hydraulic fracturing and manage the resulting wastewater. In addition, both single-stage and multistage centrifugal pumps are used for offshore applications in deep-water resources.

In the shale industry, reciprocating pumps dominate the positive displacement category. Hydraulic fracturing pumps rely on reciprocating technology for high-pressure applications. These pumps will have the highest growth. Diaphragm and piston pumps add chemicals to hydraulic fluids and transport the mixture of water, sand and other additives. Progressive cavity pumps can mix solid proppants with water and can even create artificial lift when well pressure is low. Multiphase applications in high-pressure areas are ideal for both twin screw and progressive cavity pumps in the upstream sector. New hydraulic pumping systems divert abrasive fluids away from hydraulic fracturing pumps, increasing pump life.

Flowserve specializes in process-intensive application in the oil and gas industry. Sulzer and ITT also provide engineered pumps in this market. For positive displacement pumps, Colfax, Flowserve and ITT are among the major suppliers. ITT's acquisition of Bornemann has also strengthened its offerings of positive displacement pumps.

Slower Investments

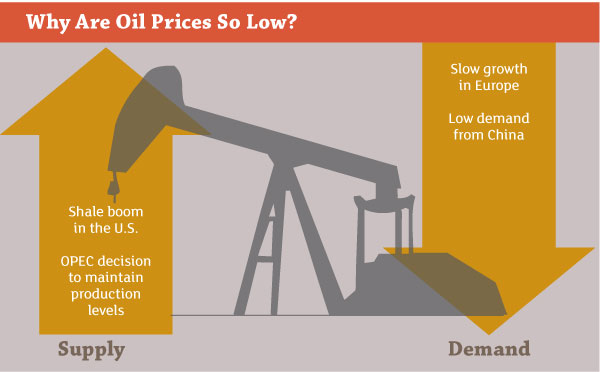

Global oil prices have been on a downward spiral during the last few months and hovered around US$45 per barrel in January 2015. The decreasing prices can be blamed on too much supply and too little demand. The U.S. shale boom and rising oil production from non-OPEC nations have glutted the market with oil from unconventional sources, while slow economic growth in the eurozone and China has lowered demand. OPEC's decision in late 2014 to not cut output or hold an emergency meeting further contributed to the price drop.

Because of their major share in international crude oil and gas exports, MENA economies are vulnerable to changes in global oil prices. However, the low cost of producing oil and gas in the region has led to economic surpluses in several countries during the last decade. These reserves have enabled Middle Eastern countries to withstand short-term upsets in global crude prices. These same countries—who are among the leading producers in OPEC—hope to retain their market share as low prices drive out other producers who cannot continue operations at the reduced crude oil price.

Several upstream projects will continue to progress for now, though at a slower pace. Saudi Aramco announced that it will renegotiate existing contracts and revisit project investments. Many other NOCs may be expected to follow suit unless there is a major decision on production levels.

Uncertain investments in upstream project development will likely dampen the demand for pumps. However, the region's constant growth in terms of population, development and consumer demand still provides several opportunities for pump manufacturers. Expanding cityscapes and the accompanying need for power and infrastructure will likely generate demand for pump installations.

The Shale Boom

In 2014, the U.S. was the largest producer and exporter of shale oil. MENA oil and gas producers, who control more than 40 percent of the global trade of crude oil and gas, see shale explorations as a direct threat to their market share. However, U.S. shale producers need crude oil prices to be higher than US$65 to US$80 per barrel to stay profitable. These producers do not have the same reserves as MENA countries to outlast the recent price drop.

While investments have slowed in the MENA region, the success of shale in the U.S. has sparked local interest in the market. Saudi Arabia has committed to exploring unconventional gas reserves. Kuwait and the UAE are reviewing the potential for shale gas developments, and Qatar is looking to end its indexation to oil prices and move to more flexible agreements. Saudi Arabia, the UAE, Oman and Kuwait have considered enhanced oil recovery for their aging fields, and the practice is expected to continue throughout the region.

What's Next?

What OPEC decides about production levels will ultimately determine the type and availability of technologies in the oil and gas sector. If the decision remains to let the market alone correct the oil price, then pump manufacturers can likely expect conservative investment plans from NOCs. Unless there is a price correction, the upstream sector will see slower developments just as MENA countries begin to consider new modes of production. Urban development may be enough to maintain activity for now.