The global, growing demand for power has softened the impact of the recent recession on the power generation sector. Going forward, this growth is expected to reach significant proportions, as evidenced by some key projected metrics and trends, including:

- A 60 percent increase in global demand for electricity by 2030, led by growth in India and China

- The literally trillions of dollars expected in infrastructure investment in the industry to 2030

- Projected growth in nuclear power, with China, Russia, India and the rest of Asia leading the way in future planned or proposed plants

These trends promise notable revenue opportunities for pumps suppliers in both new plants and existing plant upgrades and refurbishments.

Global Pump Forecast

The world's positive displacement (PD) and centrifugal pumps markets witnessed flat to negative growth in 2009, as end-user segments across the board experienced the impact of global recession. The expected strength of pump revenue growth within the power generation industry depends on regional trends.

Emerging economies, such as the BRIC (Brazil, Russia, India and China) nations, are expected to witness considerable growth over the short term of the forecast period, mainly due to infrastructure developments in these countries. Population growth, urbanization and the resulting increase in power demand will help fuel growth in the Asia Pacific.

Pump demand is also expected to increase within the power generation sector in northern Africa and the Middle East, although recovery in southern Africa is expected to be slower.

Mature economies, on the other hand, are dealing with the crippling aftereffects of the worldwide recession. Investments in plant infrastructure and retrofit needs were put on hold for the duration of the downturn. As the general economic environment improves in North America and Europe, pump revenues in this industry are expected to gradually return to moderate growth rates.

Figure 1. PD pumps revenue forecasts.

Figure 1. PD pumps revenue forecasts.In 2009, the power generation segment accounted for about 6.7 percent of the total revenues in the PD pumps market. In the same year, as shown in Figure 1, revenues for PD pumps within this industry totaled $484.7 million, with a steady growth rate expected to occur over the next few years. By 2013, the revenue growth rate for PD pumps within the power generation sector is forecast to meet or exceed pre-recession rates, at about a 6 percent revenue growth rate by 2016.

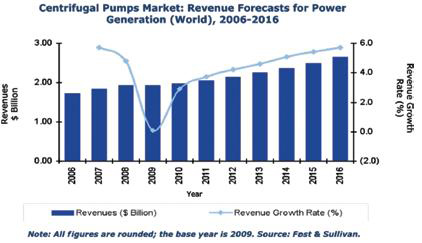

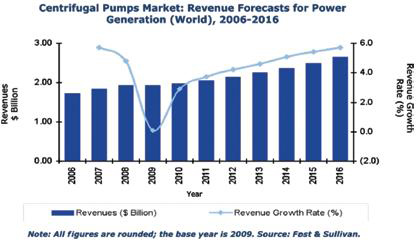

The power generation segment, in 2009, accounted for about 9.9 percent of revenues in the centrifugal pumps market. Figure 2 shows a forecast for this industry. In the same year, revenue for centrifugal pumps within the power generation market totaled $1.72 billion.

Revenue growth for this product type within the power generation industry is expected to be slightly more sluggish than revenue growth for PD pumps over the next few years. However, by 2016, the revenue growth rate is expected to return to a pre-recession level of 5.7 percent.

Figure 2. Centrifugal pumps revenue forecast.

Figure 2. Centrifugal pumps revenue forecast.Key Trends and Issues

A number of top-level trends are expected to affect pump demand in this industry throughout the forecast period, including the following positive trends:

- End-user need for environmental compliance with increasingly stringent regulations has significant impact on the market. This will continue to be a strong market driver for pumps used within the power generation industry, as well as in other industries. In addition, growing interests in alternative energy sources to counter greenhouse gas (GHG) emissions are likely to contribute to the growth.

- The focus on energy-efficiency offers a considerable potential for growth, mainly due to rising energy costs and the intense focus on driving costs out of process/production. End users are increasingly seeking the optimization of their processes to reduce energy consumption. As PD pumps are suited for applications emphasizing more efficiency, this is expected to offer a great potential for suppliers of these pumps.

- Replacements/retrofits demand will increase. Increasing investments in the water and power generation sectors over the next decade, coupled with the rising trend of PD pumps replacing centrifugal pumps in applications focused on energy efficiency, are expected to fuel the growth of the displacement PD pumps market

- Rising demand from the utility sector will continue to fuel the growth for centrifugal pumps.

Of course, challenges also exist in the industry that can impede growth, such as:

- Price pressure from low-cost participants has intensified the competition, which can push suppliers to offer higher quality, more reliable and advanced technology at competitive prices. However, the price pressure is a restraining factor on the overall revenue growth potential of the pumps market.

- Although the impact of the global recession has been somewhat mitigated for the power generation sector as a result of the rising global need for power, a short-term impact from the economic slowdown will occur as production slowly ramps up, capital expenditure resumes and excess pump inventory is sold.

- Maturity of the market: both PD pumps and centrifugal pumps are commonly used pieces of equipment for power generation, as well as many other industrial process/production areas. In mature markets, demand for such products typically flattens out over a period of time owing to consistent supply, few technological innovations and the presence of supply-side competition.

The power generation sector is a critical industry that cannot afford downtime. As such, the industry provides a consistent, if not stellar, rate of growth for the pumps industry.

In addition, the aftermarket business for pumps within the power generation sector will continue to generate growth, as plants undergo retrofits and upgrades. The opportunities for growth exist. The challenge will be identifying the fastest growing regions for the power generation sector, such as in the BRIC countries, while also taking advantage of the aftermarket opportunities in mature economies.

Pumps & Systems, December 2010