The mergers and acquisitions (M&A) activity in general, and specifically in the fluid handling industry, were at record levels in 2021, and 2022 is expected to be an active year. Valuations were at strong levels in 2021, but there could be some compression in 2022.

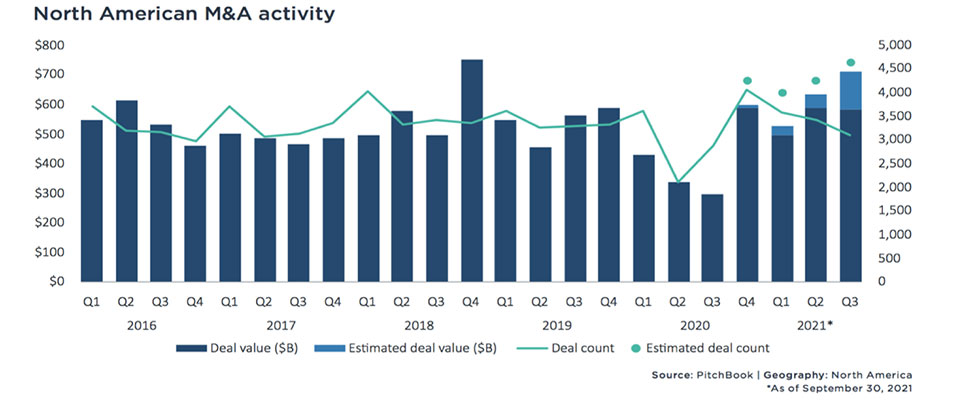

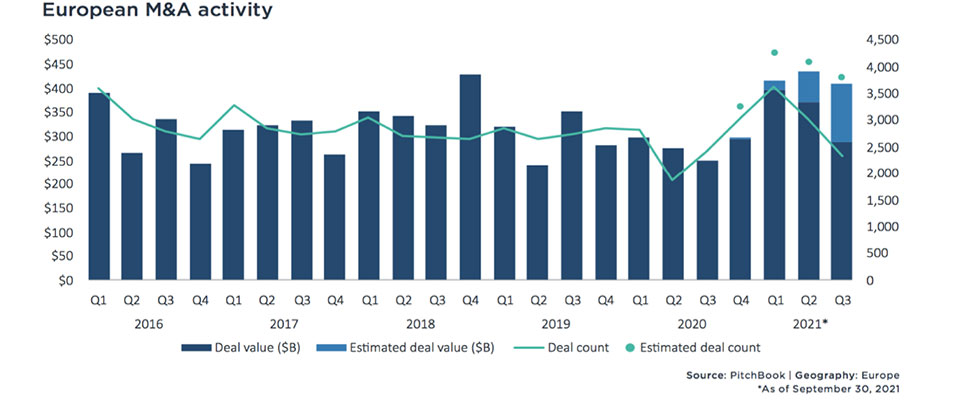

In Images 1 and 2, the line graphs indicate the number of completed transactions in a given period. The dots above Q4 2020 and Q1, Q2 and Q3 2021 indicate PitchBook’s estimated number of completed transactions after the actual data for those periods is available.

The number of transactions is a better barometer of M&A activity since the total value of transactions is impacted by multiple factors related to the mix of activity such as industries, deal size and difference in valuations between the periods. Focusing on the number of transactions, M&A activity slowed in 2020 particularly in Q2 and Q3 in North America before turning up in Q4 2020. The high level of activity continued through 2021.

Multiple factors are driving the current high level of M&A activity, and many of those factors will likely continue to drive a high level of M&A activity in 2022. On the demand side, many strategic buyers are looking to take advantage of the current low cost of debt and a high level of liquidity to pursue various objectives including growth opportunities, vertical integration, realignment of their portfolios, expansion of technology, and response to evolving customer needs and wants. Private equity buyers are driven to put record amounts of capital to work, so they are looking for new platform business as well as add-ons to existing platforms. On the supply side, some strategic sellers are looking to take advantage of the strong valuation environment to realign their portfolios.

Private equity and private business owners are taking advantage of the strong valuations to exit—or in some cases to go public. Certainly, the potential change in capital gains tax levels is an additional motivation, particularly for private business owners.

Valuations Remain at High Levels

These multiples tend to be skewed toward the high end because the financial terms for smaller and private transactions are frequently not disclosed so the database tends to be larger, public transactions. However, the trend is indicative of the market situation: Valuations dipped substantially following the 2008 financial crisis, bounced back and remained fairly consistent from 2010 to 2014 before stepping up in 2016 and remaining at that relatively high level from 2016 to 2021 (Q3).

A different look at valuation from GF Data shows multiples for private equity transactions. These are smaller-company, private transactions, and the multiples are substantially lower than the larger public company value multiples, but the trend is consistent: The M&A market remains a seller’s market as demonstrated by strong valuation multiples over the last five years, especially in the larger segments.

There is also a quality premium for companies with at least 10% per year sales growth and 10% earnings before interest, tax, depreciation and amortization (EBITDA) margin. In addition to the strong multiples, buyers have been rewarding companies with above-average characteristics with an increasing quality premium.

The valuation of any business is specific to a seller and a buyer, but there are fundamental factors that have a significant impact on valuations including:

- market demand for a specific acquisition

- potential synergies

- outlook for growth

- cost of capital

It does appear the demand for quality acquisitions is not likely to subside in the near term. However, should the outlook for growth and/or the cost of capital be negatively impacted by inflation, supply constraints or other factors, there could be compression in valuation multiples—the timing of any compression in multiples would depend on when and to what degree those negative factors become significant.

M&A Activity at Record Levels

2021 was the most active year for M&A activity in the fluid handling industry in the last five years. In fact, it was the most active year in the past 10 years. The factors driving this level of activity are the same as those driving the general M&A market activity, namely:

- growth opportunities: additional geography, expanding addressable market, etc.

- expanding technology: addressing evolving market needs and wants, e.g., asset monitoring, predictive maintenance

- integrating channels: mostly forward integration of distribution and service partners

- realigning portfolios (strategics)

- need to put capital to work (private equity)

- monetizing value creation (private equity and private business owners)

- retirement (private business owners)

However, while the activity level is strong, it is also rather concentrated in that 14 companies accounted for 65% of the activity in 2021 (through Q3 2021).

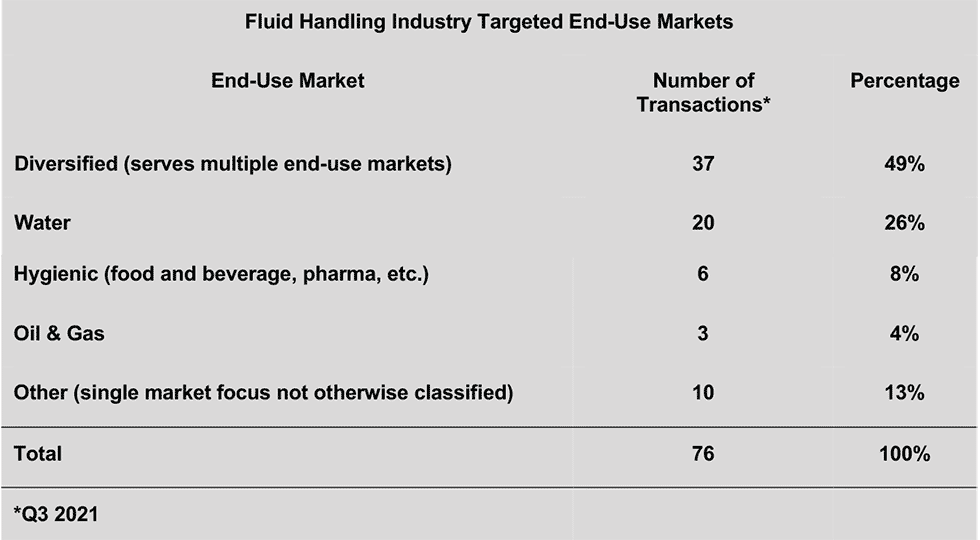

Water Most Targeted End-Use Market

Water has been the most targeted end-use market over the last few years, replacing oil and gas. Hygienic is showing up for the first time with enough transactions to be a stand-alone category—this appears to be a trend.

Thoughts About 2022 M&A

The factors mentioned earlier in the article that have been driving the demand for quality acquisitions in the industry in recent years are not likely to change significantly in 2022, barring a disruption such as experienced with the COVID-19 pandemic.

Likewise, the factors motivating potential sellers are also not foreseen to change significantly in 2022, with the possible exception that the uncertainty around the potential change in the United States capital gains tax could be clarified. There is also potential for compression in valuation multiples should the outlook for economic growth and interest rates become material headwinds in the U.S. and/or Europe.

Not all transactions are highly competitive and there are excellent opportunities for companies to grow through acquisition. However, chances are it will take a purposeful outreach program to identify those opportunities and build the relationships that lead to those opportunities.