Michael Michaud, executive director of the Hydraulic Institute, spoke with Pumps & Systems about how end users can prepare for new Department of Energy rules and policies.

Hydraulic Institute

01/13/2017

Take us through what we know and don’t know about the federal government’s pump efficiency regulations, their impact and what we can expect this year.

Early in 2016, the U.S. Department of Energy (DOE) released its commercial and industrial clean water pump (CIP) Energy Conservation Standard and Test Procedure for Pumps, essentially requiring that by 2020, pumps within scope that are sold into the market will need to be redesigned or reconfigured to meet new efficiency standards. We estimate that these requirements will eliminate some 25 percent of the pumps currently available. Certainly for pump manufacturers, this is not news as they have been preparing for this for some time. This is relatively new to most of the end users I speak with, however. They are wondering how it will affect them—if there will be a significant change to the pumps available in the marketplace and if they will need to change their procurement practices. See more of our State of the Industry 2017 coverage.

See more of our State of the Industry 2017 coverage.What do we know now about the impact of these changes?

Manufacturers are already starting to implement the changes. Many have rolled out or will be rolling out new models incorporating more efficient technologies or designs—either completed internally or acquired through some of the recent merger and acquisition activity you have reported on. So I know the pump manufacturers will be ready in 2020.Does this affect currently installed pumps or only new pumps?

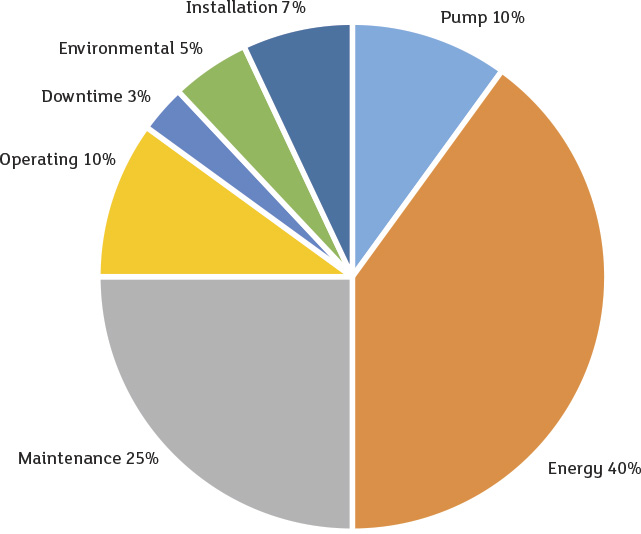

The next few years will present some very interesting options for end users. The DOE energy conservation standard does not require any change to currently installed equipment or pumps. However, as more highly efficient pumps become available in the marketplace and utility incentive programs become available, end users will have some interesting choices. When you do a life-cycle, cost-accounting analysis of pumps, most end users find that more than 75 percent of the lifetime cost of ownership is various operating costs. Energy costs alone represent the largest share at 40 percent. The upfront cost to purchase the new pump is generally only around 10 percent, with installation coming in at 7 percent. Incentives will further reduce the upfront expense, making it even more affordable to purchase a new, more efficient pump, which will have the added effect of producing more energy savings. Figure 1. Typical life-cycle cost for a pumping system (Courtesy of Hydraulic Institute)

Figure 1. Typical life-cycle cost for a pumping system (Courtesy of Hydraulic Institute)