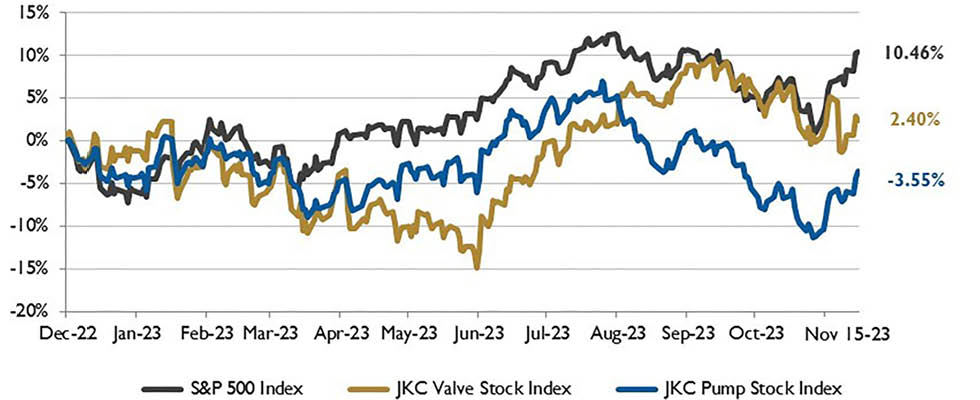

The Jordan Knauff & Company (JKC) Valve Stock Index was up 12.5% from Dec. 1, 2022 through Nov. 15, 2023, while the broader S&P 500 index was up 8.8%. The JKC pump stock index gained 15.1% for the same time period.1

Local currency converted to USD using historical spot rates. The JKC Pump and Valve Stock Indices include a select list of publicly traded companies involved in the pump & valve industries, weighted by market capitalization. Source: Capital IQ and JKC research.

Industrial production fell 0.6% in October, the largest monthly decline seen this year, due to the 10% drop in motor vehicles and parts manufacturing caused by the strikes at auto manufacturers. Vehicle production fell by 1.7 million units during the month. The United Auto Workers strike, which for the first time impacted all three major domestic automakers, ended in October. Excluding auto production, manufacturing gained 0.1%. Primary metals fell 1.7%, fabricated metal products decreased 0.1% and plastics and rubber products dropped 2.2% in October. These three manufacturing industries are major providers to the auto sector.

The Labor Department reported the consumer price index (CPI) was unchanged for the month of October from the previous month but increased 3.2% from a year ago. It was the slowest monthly pace since July 2022. The annual rate was the smallest increase since September 2021.

Energy prices declined 2.5% for the month, offsetting a 0.3% increase in the food index. Gasoline prices fell 5% in October. New vehicle prices declined 0.1% for the month, while used vehicle prices were down 0.8% for the month and fell 7.1% from a year ago. The core CPI, which excludes volatile food and energy prices, rose 0.2% for the month and 4% from a year earlier.

Ongoing OPEC+ production cuts are expected to offset production growth from non-OPEC countries and help maintain a relatively balanced global oil market next year, according to the U.S. Energy Information Administration. They forecast global liquid fuels production will increase by one million barrels per day (b/d) in 2024.

Uncertainties surrounding the Israel and Hamas conflict and other global oil supply conditions could put upward pressure on crude oil prices in the coming months. The Brent crude oil price is forecast to increase from an average of $90 per barrel in the fourth quarter of 2023 to an average of $93 per barrel in 2024. Current OPEC+ production cuts are set to expire at the end of 2024.

On Wall Street, in late November the Federal Reserve Bank released minutes showing that even though Federal Reserve Bank officials agreed a cautious approach was required in their monetary policymaking decisions, they were not ruling out further interest rate hikes. The news acted as a dampener to the markets. Mega-cap growth stocks, like tech, suffered the most.

The Federal Reserve Bank acknowledged that the economy currently faces the possibility of a recession amid still-high inflation. The Federal Reserve Bank’s key inflation indicator, the personal consumption expenditures price index, showed core inflation running at a 3.7% annual pace in September. The number has improved considerably, dropping a full percentage point since May, but is still well above the Federal Reserve Bank’s target of 2%.