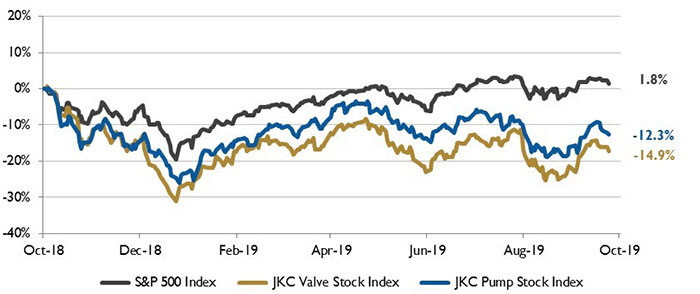

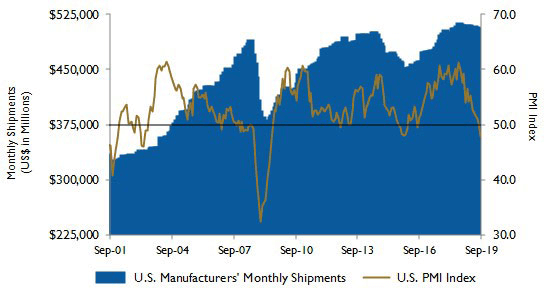

The Jordan, Knauff & Company (JKC) Valve Stock Index was down 14.9 percent over the last 12 months, while the broader S&P 500 Index was up 1.8 percent. The JKC Pump Stock Index fell 12.3 percent for the same time.1 The Institute for Supply Management’s Purchasing Managers’ Index (PMI) September reading registered 47.8 percent, a decrease of 1.3 percentage points from August. September was the second consecutive month of PMI contraction, and at 47.8 percent, the ISM manufacturing index is now at its lowest level this business cycle, including the 2015-2016 slowdown. Global trade remains the most significant issue, as demonstrated by the contraction in new export orders that began in July. Of the 18 manufacturing industries surveyed, only three reported growth: miscellaneous manufacturing; food, beverage and tobacco products; and chemical products.

Image 1. Stock Indices from October 1, 2018 to September 30, 2019. Local currency converted to USD using historical spot rates. The JKC Pump and Valve Stock Indices include a select list of publicly traded companies involved in the pump and valve industries, weighted by market capitalization. Source: Capital IQ and JKC research.

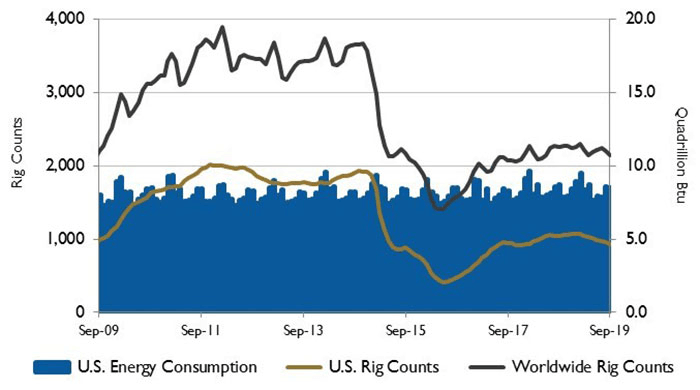

Image 1. Stock Indices from October 1, 2018 to September 30, 2019. Local currency converted to USD using historical spot rates. The JKC Pump and Valve Stock Indices include a select list of publicly traded companies involved in the pump and valve industries, weighted by market capitalization. Source: Capital IQ and JKC research. Image 2. U.S. energy consumption and rig counts. Source: U.S. Energy Information Administration and Baker Hughes Inc.

Image 2. U.S. energy consumption and rig counts. Source: U.S. Energy Information Administration and Baker Hughes Inc. Image 3. U.S. PMI and manufacturing shipments. Source: Institute for Supply Management Manufacturing Report on Business and U.S. Census Bureau

Image 3. U.S. PMI and manufacturing shipments. Source: Institute for Supply Management Manufacturing Report on Business and U.S. Census Bureau