Add ongoing and periodic costs to the buying equation.

LobePro Inc.

02/06/2018

Life cycle cost (LCC) analysis, the method used to determine total cost of ownership that involves discounting all projected cash flows to the present, is usually practiced more by industrial than municipal users. That said, while many wastewater treatment plants feel pressured to buy equipment based on the lowest acquisition price, buyers are increasingly measuring the value of quality and service by adding ongoing and periodic life cycle costs to the buying equation.

Operational & Other Cost Saving Strategies

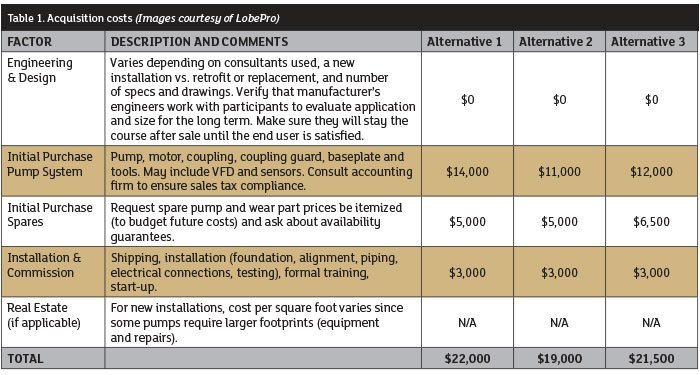

There are a number of strategies that rotary lobe pump end users in particular can deploy to reduce costs. Along with choosing a manufacturer that sizes correctly for the long term, purchasing a variable frequency drive (VFD) enables users to ramp up speed to maintain output rather than buying wear parts prematurely. Some experts say it is often wise to purchase slightly larger pumps than might be necessary for a desired flow, especially with abrasive fluids, to save money on parts by running them at slower speeds. This takes into account the exponential relationship between rotational speed and wear. It is helpful to track each pump’s efficiency, ensuring it is on the right side of the tradeoff between replacing wear parts versus higher energy costs associated with running pump motors at higher speeds. Recognize that durable parts last longer and manual compensating pressure oil bottles both consume time and are vulnerable to damage. Take advantage of designs with money saving features. These include reversible wear plates, cartridge seals with reusable holders and adjustable housing segments, for example. End users should look out for replaceable parts designed for “easy” applications accompanied by advertising that implies all applications. Send operators to training to ensure that they can properly maintain the pumps, whether changing parts, changing oil or respecting tolerances. Install inexpensive sensors that alert users of abnormal conditions. When appropriate, minimize the number of models in a plant to reduce inventory costs. Appreciate the designs that require less time to replace wear parts or rebuild free operators to attend to preventive maintenance. Reliability, ease of use, consistent pricing and part availability are the chief considerations end users value when selecting suppliers. Along with speaking to references, end users should compare warranties, ask about training, question whether every pump is tested to meet gallons per minute (gpm) and horsepower (hp) at duty point pressure, learn where repairs are made and inquire about how long and difficult it would be for two inexperienced operators to complete a rebuild. An easy way for buyers to avoid becoming vulnerable to “razor blade business models” (i.e. lower pump prices with expensive part replacements) is to request itemized wear part pricing up-front and ask about getting availability guarantees in writing. Table 1. Acquisition costs (Images courtesy of LobePro)

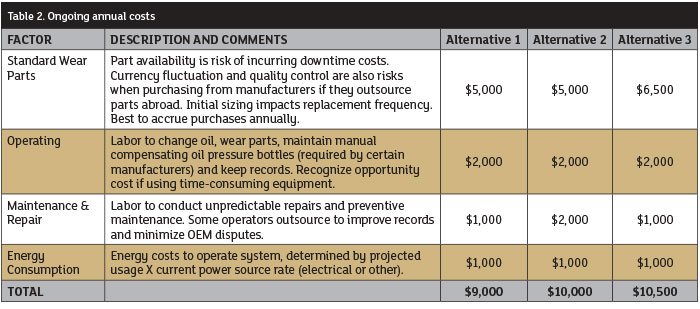

Table 1. Acquisition costs (Images courtesy of LobePro) Table 2. Ongoing annual costs

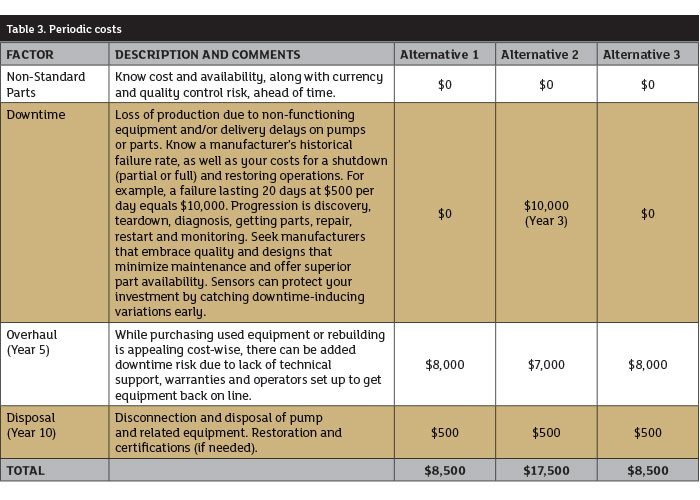

Table 2. Ongoing annual costs Table 3. Periodic costs

Table 3. Periodic costsIdentifying Pump Life Cycle Costs

The three categories of LCCs are acquisition, annual and periodic. While some factors are easier to determine than others, all are important. And while the discipline of conducting LCC analysis is not an exact science—since assigning future costs requires assumption—it is better than relying solely on acquisition costs. Three hypothetical pricing alternatives in Tables 1-3 demonstrate the impact varying cash flow factors can have on an end user’s total cost of ownership.Applying NPV Formula in Excel to LCC Analysis for Best Alternative

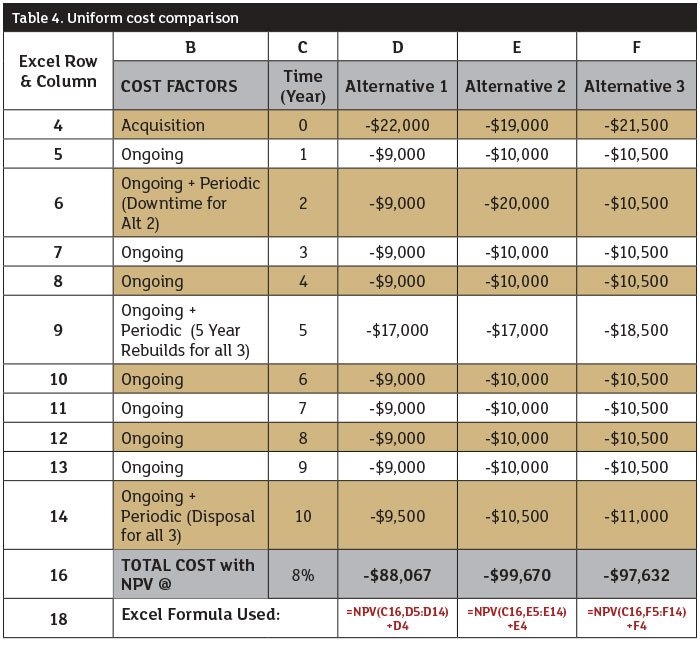

The next step in the process, after quantifying initial and future costs, is to enter them into a non-consistent cash flow net present value (NPV) formula to create a uniform cost comparison of alternatives. This formula “discounts” future cash flows because money in the future is generally less valuable because of inflation eroding buying power. The inverse is also true as future expenditures are likely to be higher due to inflation. Corporations generally use their weighted average cost of capital from debt, equity and retained earnings as a discount rate. Although NPV is generally used to identify the “highest” number derived from discounted streams of income earned less initial investment, all cash flows are negative and need to be entered as such. The best total cost alternative will be the least negative number, derived from discounted streams of future ongoing and periodic costs, added to initial acquisition costs. Microsoft Office’s Excel is an excellent tool for comparative analysis. It is possible to lay out choices in a worksheet, use built-in formulas and immediately see the impact of projection changes. For our three alternatives, let’s assume a discount rate of 8 percent and an equipment life of 10 years. Cost factors have been pulled from above and entered into Table 4. The Excel formula assumes “end of time period” cash flows. While receiving a low acquisition price is always valuable to a buyer, quality and service matter. This example highlights how Alternative 1, despite having higher acquisition costs, actually provided the end user with the lowest total cost of ownership when coupled with ongoing and periodic costs. Table 4. Uniform cost comparison

Table 4. Uniform cost comparison