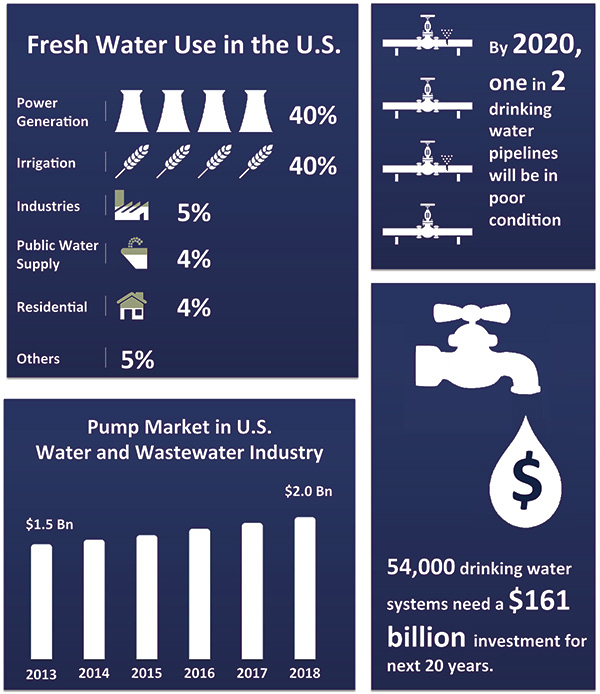

The U.S. infrastructure for the transmission, treating, storing and distribution of water requires drastic changes because of its increasing inability to sustain the new demands for potable water and water recycling. The majority of water treatment plants in the U.S. are suffering from old infrastructure technology, limited processing capacity and unpredictable weather. The overwhelming pressures on current water systems are forcing municipalities to acquire new technologies despite the funding shortages. Although the demand for infrastructure systems is undeniable, the lack of appropriate funding could undermine the ability of municipal governments to select the most technologically advanced alternatives. Many U.S. water facilities have exceeded or are exceeding their lifetimes. Because of a lack of funding, resources are constrained, which impedes the installation of the most appropriate technology. However, the absence of any investment will impose an $11 billion annual shortfall for drinking water and a $13 billion annual shortfall in wastewater. Additionally, $390 billion will be required for wastewater infrastructure systems and building new facilities in the next two decades. One program currently in place by the federal government is the Drinking Water State Revolving Fund (SRF) with $2 billion allocated for drinking water and $4 billion allocated for wastewater. Municipal governments are encouraging private investment and promoting monetary incentives to raise funds for the necessary projects. The driving factors of this initiative include new pressure from the federal government to improve water quality and safety, the increasing water supply costs because of depleted source water, a decline in the quality of raw-water, and the need to replace water distribution and wastewater collection systems for the first time. Municipal governments are also considering the population growth that is overloading current facilities in need of technology upgrades. In addition, some municipalities have developed water conservation initiatives that include setting irrigation days and creating tax and incentive programs related to environmental and residential appliance upgrades. By 2025, the U.S. is projected to have medium-to-high water stress, which is a measurement of the proportion of water withdrawal rate to the total renewable resources. This will be a challenge for water reuse management technologies that will play an important role in the future as U.S. water shortages worsen. For example, in the Midwestern U.S., aging sewers often overflow after recurring storms. Over time, this problem will impact the drinking water supply and ultimately the region’s public health. Similarly, dam infrastructure—including structural dams and non-structural runoff water management dams—suffers from flooding because of melting snow from the north. Significant upgrades are required to protect the fresh water supply and the general ecosystem from carried-down pollutants. Other states struggle with the opposite problem—water scarcity. States such as Arizona, California, Florida and Texas suffer from depleted water supplies, which are needed continued population growth, industrial manufacturing and agriculture. As many cities in these states are growing rapidly, the states must develop larger capacity to maintain the water supply demand.

The future of water in the U.S. Source: Frost & Sullivan

The future of water in the U.S. Source: Frost & Sullivan