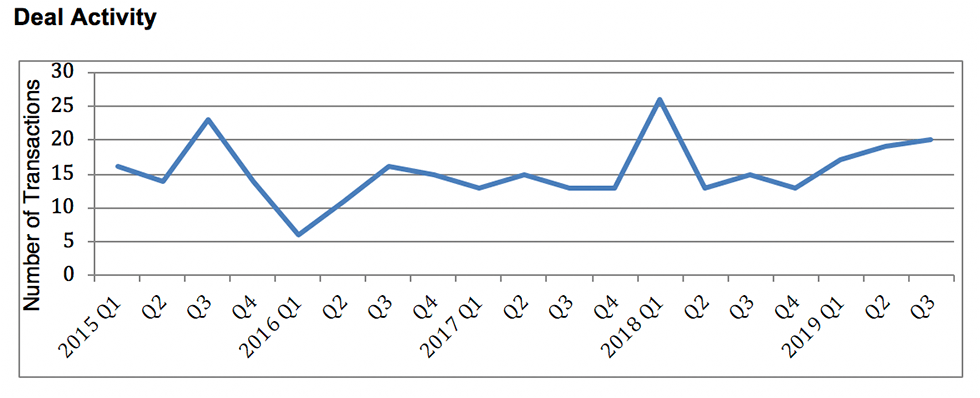

The deal activity in the industry has been strong with 56 announced transactions through the third quarter. This is the highest level of activity in the last four years and has been increasing sequentially since the fourth quarter (Q4) of 2018.

Key Factors

Strategic realignments, expanding geographic footprint and channel integration are among the key factors driving deal activity.

Valuations

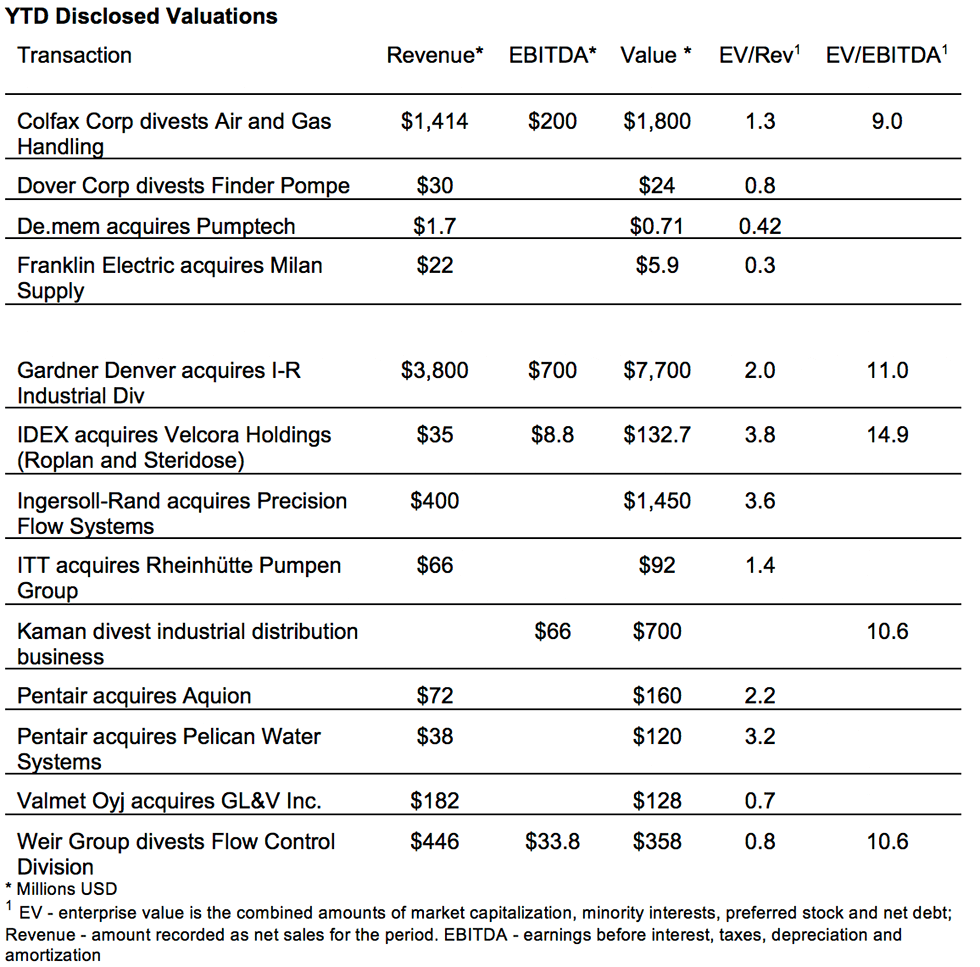

The year-to-date 2019 valuations remain very deal specific but at a high level.

The disclosed transaction valuations remain strong with year-to-date Q3 median enterprise value/earnings before interest,taxes, depreciation and amortization (EV/EBITDA) multiple of 10.8 versus the full year 2018 multiple of 8.6. The median EV/revenue multiple year-to-date Q3 2019 is 1.33 versus 1.32 for the full year 2018.

Demand remains strong for quality acquisitions with a continuation of favorable merger and acquisition conditions:

competition for deals

low cost of debt

positive long-term outlook

Notable Q3 Transactions

Kaman Corporation sold their industrial distribution business to Littlejohn & Co. for $700 million to take advantage of the current favorable market conditions and to focus on their aerospace business.

IDEX Corporation acquired Velcora Holdings AB. The business consists of mechanical seal manufacturer Roplan and hygienic mixer and valve manufacturer Steridose. The companies complement the IDEX sealing solutions as well as their health and science platforms.

AxFlow made two acquisitions in Q3 in addition to the four acquisitions they have already done in 2019. The acquisitions of the Induchem Group and Irish Pump & Valves continues AxFlow’s expansion of their distribution footprint in Europe.

May River Capital continued the build-up of their advanced material processing (AMP) platform with the acquisition of Kason Corporation.

Private equity owned Ohio Transmission Corporation (OTC) made their second fluid handling acquisition of the year with the purchase of North Carolina-based Pumps, Parts and Service.

Sulzer Ltd. continues the expansion of their aftermarket service business with the acquisition of Scottish aero-derivative gas turbine service provider Alba Power.

TechnipFMC, which was formed in 2016 by the merger FMC Technologies, a provider of subsea systems, technologies and services to the oil and gas industry, with Technip, a provider of project management, engineering and construction services, will now split into two separate companies—an integrated technology and services provider focusing on subsea and surface technologies and a separate engineering and construction (E&C) firm.

Target Industries

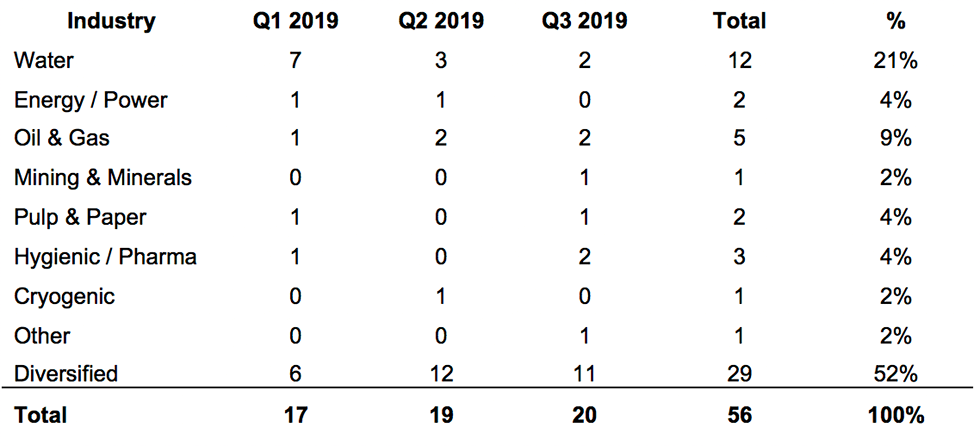

Year to date, water is the predominate industry served by target companies that have a specific industry focus. However, as the year has progressed, we have seen more diversity in the markets served by target companies.

Target Geographies

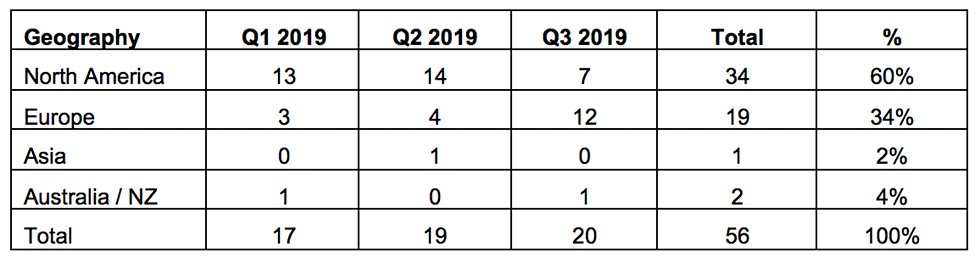

North America-based businesses have been the predominate targets in 2019, accounting for 60 percent of the transactions so far this year. However, in Q3 2019 European based targets accounted for the majority of the transactions—most of those transactions (67 percent) were inter-Europe transactions (buyer and seller were both European).

Thomas E. Haan is the principal of Global Equity Consulting LLC, providing business development services to midsize manufacturing, distribution and service companies in the fluid handling industry. He is also an operating director for City Capital Advisors, an M&A advisory firm based in Chicago. Haan has more than 40 years of experience, primarily in senior management roles for manufacturing companies serving the process industries. His global experience includes involvement with mergers, acquisitions, joint ventures and their integration. He has lead negotiations as well as the integration of joint ventures and acquisitions in Saudi Arabia and South Korea, Australia and New Zealand. Haan has extensive experience in P&L management, strategic planning and global business development. He is the former president of EagleBurgmann Industries, LP, and the Fluid Sealing Division of Flowserve Corporation. His experience also includes positions as a board member, senior vice president of international operations and director of sales. He has served as an appointee of the U.S. Secretary of Commerce on the Michigan District Export Council, past president of the Fluid Sealing Association, as well as chairman of the Associate Member Council and a member of the Board of Directors of the Hydraulic Institute. Haan is a graduate of the School of Business of Western Michigan University.

In this webinar, we’ll explore how engineering teams use PIPE-FLO to design, model and validate water-based systems that optimize energy usage, scale with operational growth, and maintain long-term durability.

Learn how electrical signature analysis (ESA), machine learning and pump digital-twin models work together to identify pump-specific faults and performance issues and much more.

Attendees will see a live showcase of technology defining the modern plant floor, from AI-powered translation to GPS and team-wide safety alerts and much more in this webinar..