Water scarcity presents a serious challenge to individuals, communities and industries around the world. The statistics are startling: Water demand exceeds supply in regions that are home to more than 40 percent of the world's population. Currently 660 million people do not have access to improved sources of drinking water, and a billion do not have electricity. By 2025, an estimated two-thirds of the global population will not have access to clean water, and by 2050 the world will demand 55 percent more water and 70 percent more energy. According to the United Nations, the world's population is projected to grow from today's 7 billion to 9 billion by 2040. That growth—combined with trends in urbanization, mobility, economic development, international trade, cultural and technological changes, and climate change—is driving increased competition among water, energy, agriculture and other sectors. Companies in water- and energy-intensive industries have an increasing interest in evaluating and managing the risks while identifying opportunities associated with the interdependencies of water and energy.

The Water-Energy Nexus

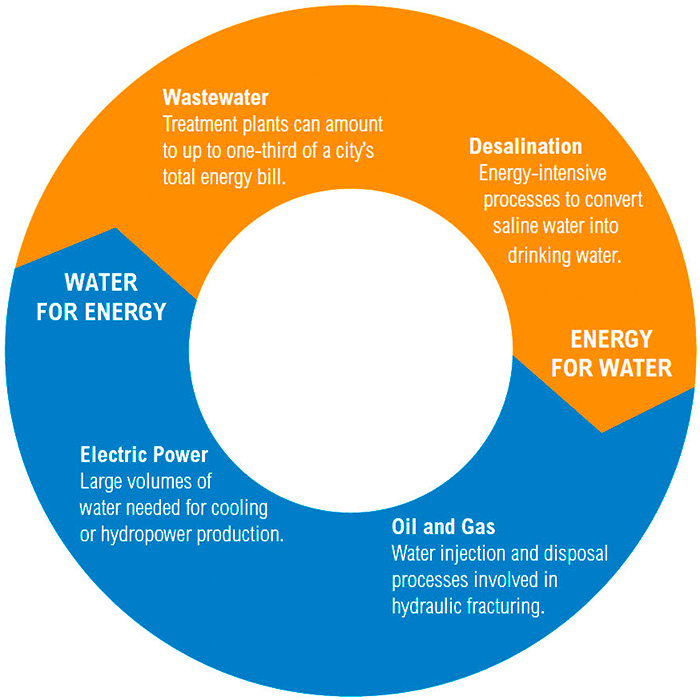

Water and energy resources are interconnected in what is referred to as the water-energy nexus (see Figure 1). Significant amounts of freshwater are needed to cool thermoelectric power plants, drive turbines that create hydropower, and extract and process oil, gas, coal, metals and chemicals. Similarly, significant energy resources are needed to heat, treat, desalinate and transport water. Figure 1. The water-energy nexus shows the connections between these two crucial resources. (Graphics courtesy of GE)

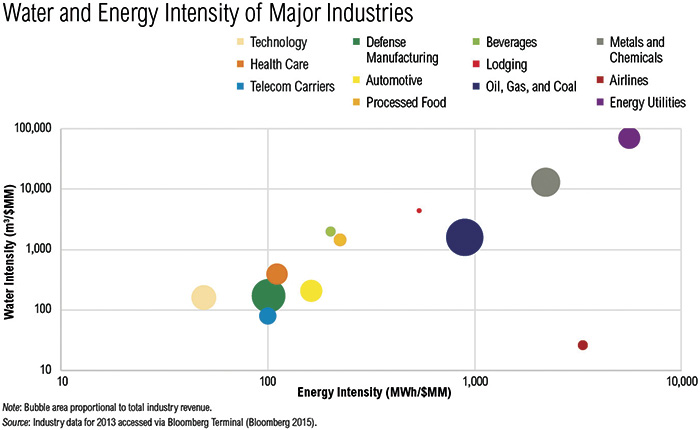

Figure 1. The water-energy nexus shows the connections between these two crucial resources. (Graphics courtesy of GE) Figure 2. Water and energy intensity of major industries

Figure 2. Water and energy intensity of major industries Business Risks & Rewards

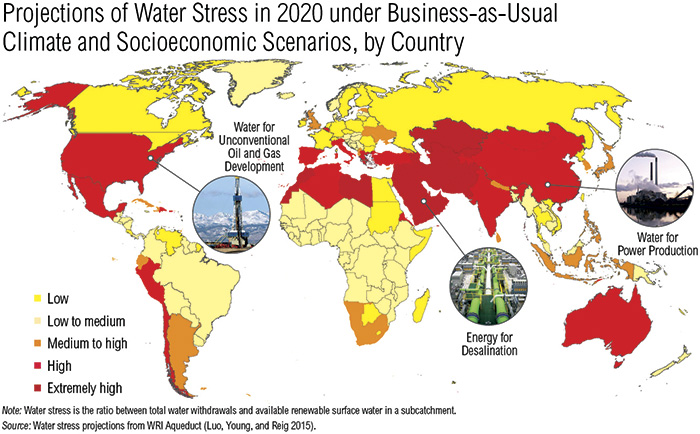

Companies can look to industries and regions now facing risks at the water-energy nexus for insights on the challenges coming to their own regions or value chains. Increasing demand for water and energy is forcing tradeoffs in arid or water-stressed areas like the Middle East and North Africa (MENA), the U.S. and China. Industries that face risks related to water and energy supply are already finding emerging solutions to address their reliance on scarce resources. MENA countries face extreme water stress and are using oil and gas to power desalination plants in an effort to address the widening freshwater supply gap. One country is projected to use all of its current energy production for desalination by 2035. To meet future needs, water providers will need desalination solutions that increase energy efficiency and tap cleaner energy sources. They also need to look for innovative, affordable water solutions beyond desalination. As China builds new power plants to meet future electricity needs, the country is confronting tradeoffs between energy and power—water scarcity becomes a risk as the country builds more power plants. China is home to the world's largest fleet of thermoelectric power plants, most of which are coal-fired and require a significant supply of freshwater for cooling. Nearly 60 percent of China's coal-fired power generation is in regions that face high or extremely high water stress. Water scarcity is likely to become an increasingly important risk factor for power providers to manage, and they are exploring opportunities to reduce their reliance on scarce freshwater resources. Figure 3. Projections of water stress in 2020 under business-as-usual climate and socioeconomic scenarios shown by country

Figure 3. Projections of water stress in 2020 under business-as-usual climate and socioeconomic scenarios shown by countryOperating at the Water-Energy Nexus

Risks and opportunities in these regions are a wakeup call to other regions. Industries and regions currently facing risks offer a high-level checklist for companies operating at the water-energy nexus:- Acknowledge risks to supplies of water and energy, but don't overlook solutions that address demand.

- Take full advantage of water conservation, water reuse and energy recovery.

- Shift demand to alternative water options and clean energy resources.

- Create new partnerships and business models.

New Ideas & Approaches

Instead of trying to expand the supply of limited freshwater and fossil fuel resources, companies can find opportunity in reducing demand and scaling alternatives. Some options include:- Inclusive approaches that recognize the benefits of gender mainstreaming and local stakeholder engagement in water and energy resource decisions

- Ambitious cross-sector goals for end-use energy efficiency, water reuse, decentralized clean energy and smart infrastructure

- Financial due diligence with innovative approaches to pricing carbon and valuing water