01/29/2016

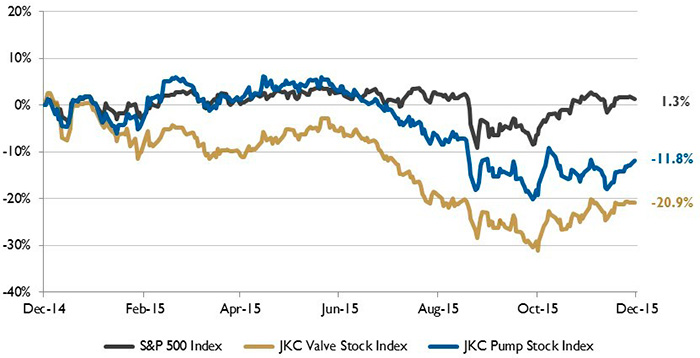

The Jordan, Knauff & Company (JKC) Valve Stock Index was down 20.9 percent over the last 12 months, while the broader S&P 500 Index was up 1.3 percent. The JKC Pump Stock Index also decreased 11.8 percent for the same time period.

Figure 1. Stock indices from Dec. 1, 2014, to Nov. 30, 2015 Source: Capital IQ and JKC research. Local currency converted to USD using historical spot rates. The JKC Pump and Valve Stock Indices include a select list of publicly traded companies involved in the pump and valve industries weighted by market capitalization.

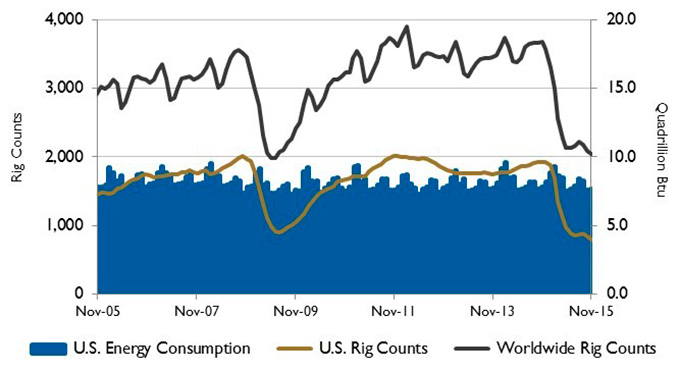

Figure 1. Stock indices from Dec. 1, 2014, to Nov. 30, 2015 Source: Capital IQ and JKC research. Local currency converted to USD using historical spot rates. The JKC Pump and Valve Stock Indices include a select list of publicly traded companies involved in the pump and valve industries weighted by market capitalization. Figure 2. U.S. energy consumption and rig counts Source: U.S. Energy Information Administration and Baker Hughes Inc.

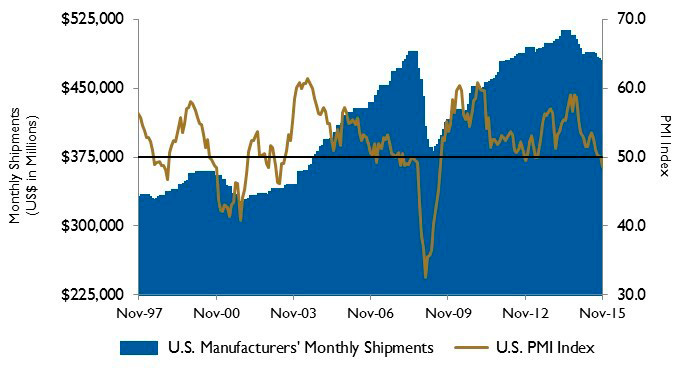

Figure 2. U.S. energy consumption and rig counts Source: U.S. Energy Information Administration and Baker Hughes Inc. Figure 3. U.S. PMI and manufacturing shipments Source: Institute for Supply Management Manufacturing Report on Business® and U.S. Census Bureau

Figure 3. U.S. PMI and manufacturing shipments Source: Institute for Supply Management Manufacturing Report on Business® and U.S. Census BureauThese materials were prepared for informational purposes from sources that are believed to be reliable but which could change without notice. Jordan, Knauff & Company and Pumps & Systems shall not in any way be liable for claims relating to these materials and makes no warranties, express or implied, or representations as to their accuracy or completeness or for errors or omissions contained herein. This information is not intended to be construed as tax, legal or investment advice. These materials do not constitute an offer to buy or sell any financial security or participate in any investment offering or deployment of capital.