Electric drives are used in various applications in the oil and gas industry for varying motor speeds driving critical components, including pumps, fans and compressors. Both AC and DC drives are used, but AC units dominate most applications. This article explores some of the recent trends and issues in the European electric drives market.

Key Market Issues

Certainly the area of most concern for drives suppliers has been the severity of the current economic downturn in Europe. While the oil and gas industry has been a bit more resilient than some other hard-hit industries (such as automotive or chemical), a number of issues continue to challenge demand for drives in this sector.

One is the need for customized motion control solutions. The oil and gas industry employs high powered drives for highly critical applications like drilling or pump rod applications. In many cases, systems have to be customized to suit the requirements. Such applications require special drives with added intelligence or controls for additional parameters, apart from speed/torque. In addition, power and voltage requirements vary with the demands of the application and in most cases the drives have to be specially designed and manufactured. The need to manufacture drives that are scalable for different applications, yet reliable, has increased. The challenge for suppliers is to successfully deliver the drive solution with the least possible lead time.

A further issue confronting suppliers is the declining price trend for variable frequency drives (VFDs) over the past few years, largely based on increasing competition. End users demand more value-added features in drives without price premiums attached. Customers expect more flexibility and features like software for streamlining installation procedures, self-diagnostics, etc. This has been a common issue for technology upgrades across a variety of industrial segments for years-end users demand "bells and whistles," but will not pay for them. This can create a drag on technology advancement and limit the ability of suppliers to command higher margins.

The current state of the oil and gas industry in Europe is another challenge. Declining investments due to drops in crude oil prices have resulted in the shelving of many projects, with drive sales expected to be negatively impacted in the short term of the forecast period.

Additionally, most of Europe's oil production has been from countries like the United Kingdom and Norway that form the North Sea belt. This region, where exploration and production activities started as early as the 1970s, has been experiencing depletion of its reserves, and new field discoveries are minimal. The maturity of many oil wells contributes to decreases in output. Although maturing wells give rise to improved oil recovery techniques and improved drive sales, the lack of new reserves remains a restraining factor. If new oil reserves are not found, Europe's external dependence on oil supply could result in a fall in the internal energy market.

While some serious issues create barriers to the demand for electric drives, some factors create promise in the market.

The aforementioned enhanced oil recovery techniques for maturing wells are expected to support demand for pumping applications for progressive cavity pumps (PCP), electrical submersible pumps (ESP) and sucker rod pumps (SRP). This demand, in turn, is expected to increase the demand for energy saving electric drives.

There is also the sheer volume of demand, as the European Union is the second largest oil and gas consumer after the United States. With the consumption of gas forecasted to increase in the future, the need to import gas from major gas producing countries like the United Kingdom, Russia, the Netherlands and Norway has only risen.

Europe imports almost one-third of its gas from Russia. To meet the demand, huge sums are expected to be invested for the development of pipelines. With a growth in the length of the gas pipelines, the need for large compressors to compress the gas will increase as will the need for high powered drives with power ratings of 30 MW to 40 MW. The pipeline projects also have pump applications to transmit the fluid (oil or gas) through them, which will increase the demand for electric drives for pump applications in the pipelines.

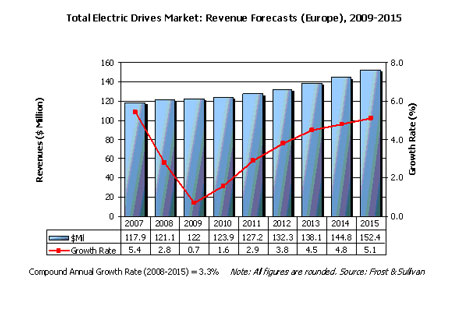

European Market Forecast

The following graph shows the forecast for the total electric drives market in Europe from 2009 to 2015. The base year is 2008.

|

| Figure 1 |

The short-term market is expected to exhibit weak growth, but improvements in the global economy are anticipated to help lift growth back to more familiar territory by the end of the forecast period. Of the base year revenues, drives used for pumps accounted for approximately 64 percent of the total, with compressors and fans at 20 percent and 16 percent, respectively.

Pumps are the major applications for drives in this market. Pumps in the oil and gas industry are used across all end user applications (upstream, midstream and downstream). The majority of the high power-rated drives for pumps are used for oil exploration purposes where high powered motors are used. In midstream applications, large mainline pumps are used to transport oil and gas. Refineries are another major consumer of pumps and drives.

As global economies begin to rebound slowly in 2010, the oil and gas sector in Europe is expected to once again be a growth market for electric drives suppliers.

Pumps & Systems, January 2010