Pump sales will increase as developing nations expand production to meet demand.

While many variables affect the dynamics in global power generation, four major trends drive notable growth in the power market. They include:

- Energy demand globally is expected to increase 1.4 times by 2030.

- Global gross domestic product (GDP) is expected to rise 3 percent by 2030.

- Regulations are and will drive the need to cut emissions two fold by 2030.

- Smart grid technologies promise to reduce future power consumption by approximately 20 percent.

The pull between the need to increase production capacity and the push for conservation promises a dynamic market throughout the next 10 to 15 years. This, in turn, portends good revenue growth prospects for pump suppliers.

Two key sectors in the power generation market are coal (which will still have a prominent position) and nuclear power. This article provides a brief overview of these two sectors to reflect which critical trends and issues are expected.

Coal Power

Coal-powered thermal generation will retain its top spot up to 2030, despite advances in natural gas production and renewable sources. World net coal-fired generation is expected to increase from 8.26 trillion kilowatt hours (kWh) in 2010 to 12.9 trillion kWh in 2030—an increase of 56 percent. Most demand will come from developing nations in Asia as they strive to meet growing demand. Coal is one of the top three fastest growing electricity sources. However, the abundance and lower emissions offered by natural gas generation could present a significant challenge to coal’s future dominance.

|

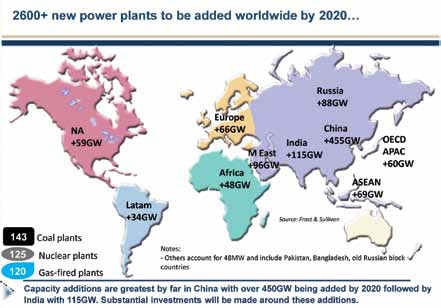

| Figure 1. Power plants added worldwide by 2020 |

Looking at a regional picture, European imports of coal will begin to decrease after 2015 because a switch to natural gas generation and renewable sources will take place as mandated by Europe’s 20/20/20 policy. Asian coal imports will take up any slack caused by decreasing consumption elsewhere as imports are set to increase at a compound annual growth rate (CAGR) of 1.69 percent to 2030. Australia and Indonesia are the main coal exporters to Asia, which will increase imports into the future to meet rising demand. China and India’s power generation from coal more than doubles by 2030, dwarfing any other region except the Association of Southeast Asian Nations (ASEAN), which grows at 3 percent per year.

Nuclear Power

While the majority of the world’s electricity demand will continue to be met by coal, the nuclear sector has also been a hot area of discussion for some time.

Nuclear generation is attracting new attention as countries look to diversify their energy portfolios and provide a low-carbon alternative to fossil fuels. Safety, waste disposal and rising construction costs continue to dampen the development of nuclear power. Developed nations—such as the European Union (EU) and U.S.—currently have the largest installed base of nuclear power, generating 0.9 and 0.82 trillion kWh respectively.

Nuclear power accounted for 14 percent of the global electricity supply in 2010. This will decrease to 13 percent by 2030 because of faster growth from renewable resources and fossil fuels. The highest growth rates will be in India and China as they continue to diversify to meet rising demand.

With the addition of third generation units, China is fast becoming a leading global innovator for nuclear power generation. This innovation will help modernize nuclear power. Russia continues to invest heavily in nuclear power as it looks to export natural gas reserves and its nuclear goods and services.

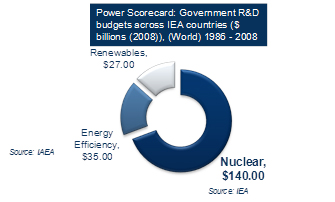

Many countries are still pursuing nuclear power after the Fukushima incident, although with safety as a prime concern. This increases lead times and required investment, hindering growth. Even with the demise of new orders and the rise of other technologies, nuclear continues to receive R&D funding from the government (see Figure 2).

|

| Figure 2. Government funding of power |

Pumps in Power Generation: Outlook

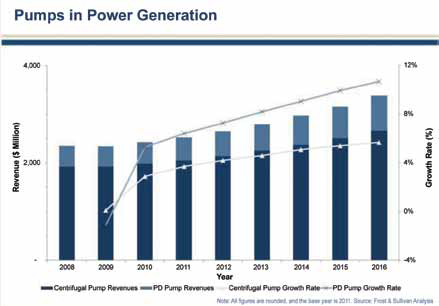

The forecasted growth is fairly robust for pump revenue in the global power generation sector (see Figure 3). The trends driving growth in power demand and infrastructure will be a boon to pumps and pump systems through the short- and mid-term (the forecast period goes to 2016).

|

| Figure 3. Total pump market: revenue forcasts for power generation, 2008 - 2016 Global |

Regionally, Europe continues to be challenged with economic issues, so growth in that region for pumps in the power segment is expected to be repressed for most of the forecast period, likely around the 1 to 2 percent range. Stronger pump revenue growth rates (and therefore greater opportunity) are expected in the Middle East (5 to 10 percent, including the thriving desalination market that incorporates a significant energy play typically), North America (4 to 7 percent) and Asia.

Within Asia, varying pockets of opportunity exist for pump suppliers, depending on the country of focus. Indonesia, for example, is expected to quintuple its electricity consumption by 2030. The opportunity that this demand will generate for pumps is significant, as new infrastructure will be needed to accomplish provision of adequate supply.

The Chinese engine, of course, continues to hum. By 2015, power generation in China is expected to surpass that of North America. Though the Chinese pump market is highly fragmented, increased demand will benefit suppliers across the board. India’s power development is driven by capacity shortages, growing electrification and power industry liberalization. Its percentage of the world’s electricity output is expected to almost double by 2030. Major North American pump suppliers have responded to this potential by increasing their manufacturing presence in that country.

A further interesting region for future opportunity is Africa. The key driver for the development of the African power generation market is a shortage of generation capacity, particularly prevalent in Sub-Saharan Africa. This is expected to prompt substantial investments for new capacity, which bodes well for pump demand in the region through the next decade. The political volatility of the region, however, means that pump suppliers tread cautiously when considering investments.

Continually, one of the top five industry verticals to use pumps extensively in operations, the global power generation industry is expected to provide promising growth during the next 10 years. Emerging economies will be the biggest engines of growth, with coal plants continuing to dominate the landscape. Innovation in the nuclear industry, however, promises a strong potential for future growth.