Since the 2009 recession, the refining sector has fallen on tough times. During the next 10 years, operators at one in three refineries in North America are expected to struggle to keep up with ever-changing global conditions, unless they restructure operating models.

In 2013, the average price of gas increased by almost 10 percent, primarily because of the refinery closures. The price of Brent crude is at $120 per barrel as opposed to West Texas intermediate (WTI) crude, which sells at $106 a barrel. Also, the demand for gasoline is at a 15-year low. Some refineries do not have access to cheap natural gas, which is a crucial raw material. However, with the depressed market demand, some refineries are challenged with passing escalating prices onto customers.

Other factors also cast a pall on the future of the refining industry in North America. Several major refineries, in the U.S. and Canada, have shut down. Since December 2013, 4 percent of the refining capacity in the U.S. has been lost. Two large refineries that accounted for about 20 percent of the Northeast’s gasoline production closed.

In January 2013, Hovensa shut down a plant in St. Croix that was processsing approximately 350,000 barrels of crude per day. During the last seven years, two refineries in Oakville and Montreal, Canada, have closed. In addition, if no buyers can be found, Imperial Oil Ltd. will close its unit in Dartmouth.

The refinery closures in the U.S. and Canada can be linked to many causes. The Canadian refining industry is facing stringent rules because of an aggressive move by the federal government that forces refineries to reduce green-house gas emissions and other pollutants. The Canadian refining industry warned the government that such regulations would result in refinery closures in Eastern Canada, with the loss of hundreds of jobs. It is also predicted that even without such regulations, the Canadian refining industry would witness the closure of one in nine refineries, with three others at risk.

The situation is similar in the U.S. The East Coast has older refineries that process Brent sweet crude, which is priced higher than WTI. These refineries also lack access to cheap natural gas, a vital raw material for refineries. While Brent crude is excellent for gasoline and middle distillate production, the demand for gasoline has decreased dramatically. These factors have significantly affected refineries, so much so that they are running at about 60 percent capacity. Also, these refining capacities face stiff competition from refineries in the Great Lakes and midwest that are running at 95 percent capacity. In states such as New Mexico, Utah, Montana and Colorado, this is reflected in comparatively cheap gas prices. Access to cheap natural gas and WTI makes refineries in the midwest and Gulf Coast relatively profitable to operate.

Pump Market Outlook

Pump demand in refineries was hit hard during the recession, evident in the abatement in pump orders. Not only was the expansion of refineries during the recession negatively affected in North America, plants were also not operating at full capacity. The North American refining industry is experiencing a major transition because of significant challenges, making investors reluctant to increase financial stakes in the industry. They have begun to look elsewhere, investing in high-growth areas, such as the Middle East and Asia.

Since the refinery sector is a mature industry for pumps, factors such as replacements, retrofits and automation will help drive the growth of pump demand. Refineries in the East running at about 60 percent capacity, while others are shutting down, portends weak demand for pumps.

In the short term, the most promising areas for pump manufacturers are in the Midwest and Gulf regions, in which refineries continue to operate at strong capacities. In these areas, the industry is experiencing the expansion of facilities to compensate for the loss in capacity in the East. Therefore, these facilities support the three pillars of replacements, retrofits and automation, which balances much of the weakness that is evident in other U.S. regions. Canada continues in a similar situation, wherein closures and expansions of facilities tend to balance the demand for pumps.

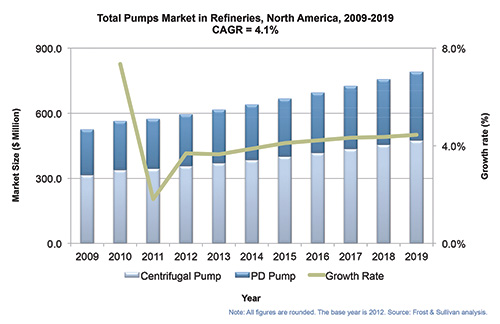

As evident in Figure 1, soon after the recession, the commencement of projects that were put on hold or postponed in 2009 created a sharp increase in demand for pumps. This resulted in a growth rate of more than 7 percent in 2010. The factors discussed in this article affected the drop in the demand for pumps in 2012, and this trend is expected to continue in 2013.

The growth rate in 2012 for pumps in refineries was about 3.7 percent. The revenue of pumps in refineries is expected to reach $790 million by the end of the forecast period with a compound annual growth rate of 4.1 percent. The North American split between positive displacement (PD) and centrifugal pumps continues to remain at 60 to 40 percent, but the demand for PD pumps is expected rise in the future.

Figure 1. Refinery pump market overview

Conclusion

Refining capacities in North America are at the mature stage. With the closure of refineries in North America and expansion of some profitable refineries, the overall market offers pump manufacturers limited growth opportunities. As a result, suppliers are looking for opportunities created by the changing oil and gas landscape—including shale oil and gas, the expected growth in micro liquiefied natural gas plants and other similar areas. These are areas that offer some promise of increasing pump sales, while the refinery sector continues to exhibit weakness for the foreseeable future.