The market's bright future in North America

The proverbial “when one door closes another starts to open” is transforming the services industry. Pump manufacturers are looking at the service industry in a whole new light as pump industry growth slows and the servicing industry growth rate surges ahead. The pump market is in a mature stage with nominal growth expected, while the service industry is expected to grow at a stronger rate.

This can be attributed to a quantum change in thinking at the shop floor and management level, with plant managers and executives realizing that the initial cost of purchase of a pump is just a fraction of the total cost of ownership (TCO), which includes the installation, repair and maintenance, field testing and other inherent costs.

The service industry targets the same end-user segments as the pump industry including, but not limited to:

- Oil and gas

- Food and beverage

- Automotive

- Power generation

- Chemical

- Pharmaceutical

- Water and wastewater

This “Business of the Business” provides an overview of the North American pump service industry, addressing trends that can benefit the industry as a whole and at the manufacturer and service provider level.

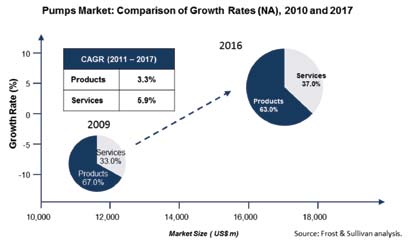

Figure 1. Pumps Market—comparison of growth rates (NA), 2010 and 2017

Growth Trends

The service industry can be differentiated by the type of services offered and the service provider. Types of services can be segmented. See Table 1.

Table 1. Pump service market—types of services (North America), 2010

The recent upswing in the North American pump service market can be attributed to several factors. One factor is that the pump market is in a mature stage with major installations already in place. This past-installed base is aging and needs to be replaced or upgraded eventually. The replacement of older pumps is a key driver for the installation and commissioning market, while the refurbishment and spare parts for existing pumps is a key driver for the maintenance, repair and overhaul (MRO) market because the older equipment becomes, the greater the likelihood of repair needed.

Another key factor driving the market is the need for improved plant profitability. Manufacturing and process plants need to minimize waste due to leaks or under performance and maximize return on investments (ROI) by:

- Investing in newer products that offer higher energy savings

- Adopting software solutions that aim to increase efficiency at a plant level

The need for improved plant profitability is driving the market for smart pumps and condition monitoring equipment. Many end users are increasingly adopting these technologies to reduce operational expenses while improving performance, therefore increasing the return on assets (ROA). The current trend is to move from adoption of equipment-specific solutions to the adoption of plant-wide solutions, which provide better control and improved monitoring. These solutions help predict issues and repairs that might be needed using a historic-data based statistic model, helping minimize downtime. As the product and the solution need a high level of customization, it gives an impetus to the servicing and installation market.

In addition, North America is facing a talent crunch of skilled technicians. As a result, maintaining an in-house service unit is becoming a difficult proposition for end users. In this scenario, end users may look to outsource their service needs as they can no longer afford to maintain this infrastructure in-house. At the same time, there are a few factors that are expected to negatively impact the growth of the service industry in the near to long term.

End users of rotating equipment tend to be late adopters of the newer technologies that would require enhanced services such as condition monitoring, intelligent pumping and electronics integration. As of now, limited numbers of end users in process industries are experimenting with these solutions, and end users in the discrete manufacturing segment are yet to adopt these solutions.

Over the near-term, poor credit availability and difficult economic conditions due to the debt crisis in regions of the European Union (EU) limit the attractiveness of major capital projects for industrial firms, hurting the installation and commissioning market and related service offerings like optimization and consulting services. The long-term decline of the industrial base in the U.S. and Canada is due to the compelling cost savings of outsourcing manufacturing to emerging economies. This affects the installed base of pumps, which in turn hurts the long-term growth for other service offerings as well.

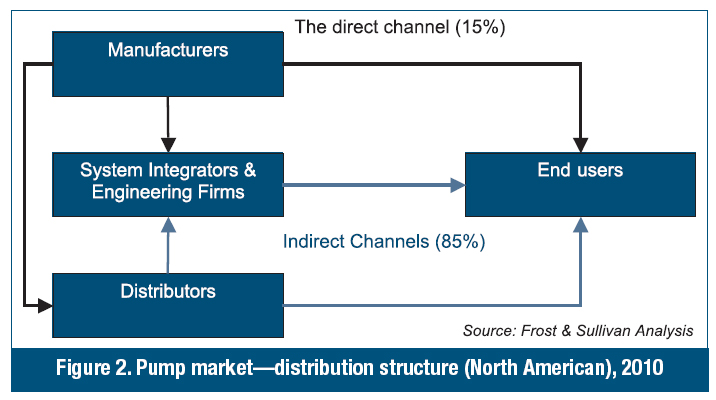

Figure 2. Pump market—distribution structure (North American), 2010

Service Channel Analysis

The key point of sale for most of the end-user segments are the distributors. Nearly 80 percent of the sales occur through distributors. Their local presence coupled with their quick response time makes them the preferred contact for end users. It comes as no surprise that the first point of contact that end users turn to for their service requirements are distributors.

Because the pump service market is expected to offer higher growth potential than the pump market, many new players are entering the market. Pump servicing is a key deliverable for distributors. Distributors build their reputations with end users through quality servicing, which helps with lead generation. Understanding this, few pump companies have started manufacturing pump parts and servicing other manufacturers' pumps. This helps distributors provide service to other pump brands and increase market penetration. Another key entrant to the market is automation vendors who provide condition monitoring and wireless and smart pump solutions to end users. In addition, participants from other industries—such as seal manufacturers—are joining the bandwagon by providing asset management solutions for pumps, valves and other machineries that use seals.

Future Growth Market

The service industry promises to grow during the next decade. With opportunities for increased service revenues for manufacturers and distributors, value chain providers continue to increase their expertise and scope to address customer needs.

Pumps & Systems, December 2011