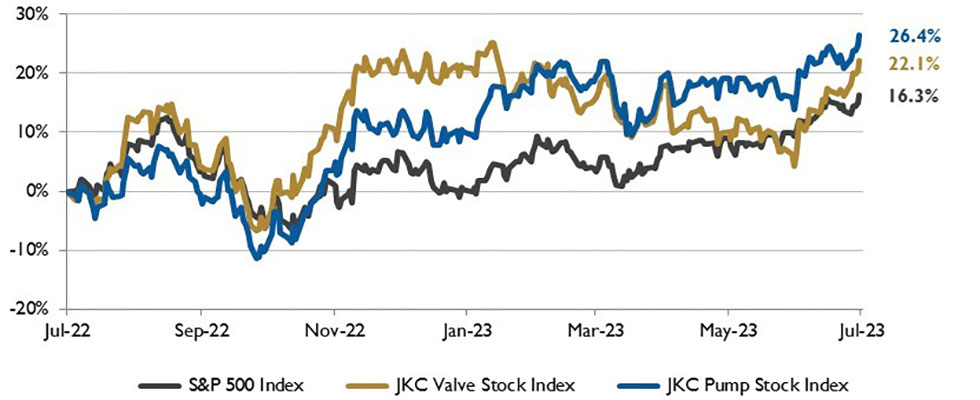

The Jordan Knauff & Company (JKC) Valve Stock Index was up 22.1% over the last 12 months, while the broader S&P 500 index was up 16.3%. The JKC pump stock index gained 26.4% for the same time period.1

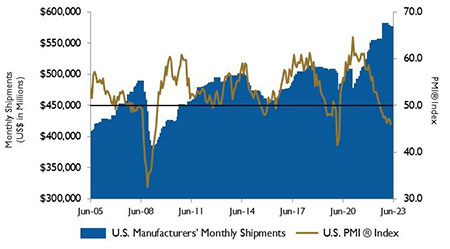

The Institute for Supply Management’s Purchasing Managers Index (PMI) fell to 46.0% in June, showing the manufacturing sector contracted for the eighth consecutive month. Overall production saw one of the largest declines, falling 4.4 points to 46.7%, marking its lowest reading since May 2020. The New Orders Index rose to 45.6%, indicating orders are still contracting but at a slower rate than in May. The Prices Paid Index slipped to 41.8% as manufacturing price growth continued to contract. The Customers’ Inventories Index dropped into “too low” territory (46.2% versus 51.4%), a positive sign for future production.

Local currency converted to USD using historical spot rates. The JKC Pump and Valve Stock Indices include a select list of publicly traded companies involved in the pump & valve industries, weighted by market capitalization. Source: Capital IQ and JKC research.

Orders for durable goods increased for a third straight month in May gaining 1.7%. Orders for all transportation equipment rose 3.9%, amid a solid 2.2% gain in motor vehicles and parts as the hard-hit auto sector continues to rebound. Nondefense aircraft orders increased 32.5%. Excluding transportation, durable orders were up only 0.6%.

Last year, global trade in liquefied natural gas (LNG) set a record high, averaging 51.7 billion cubic feet per day, a 5% increase compared with 2021. Liquefaction capacity additions, primarily in the United States, drove growth in global LNG trade. At the same time, increased LNG demand in Europe also contributed to trade growth as LNG continued to displace pipeline natural gas imports from Russia.

Source: U.S. Energy Information Administration and Baker

Hughes Inc.

The U.S. imported 9% more crude oil from Mexico and paid more per barrel in 2022 compared with 2021. The U.S. did not export any crude oil to Mexico in 2022. As global crude oil prices rose substantially in 2022, the 9% volumetric increase corresponded to a 47% value increase in U.S. crude oil imports from Mexico last year compared with 2021. Mexico is the largest export market for U.S. petroleum producers; nearly 20% of all U.S. petroleum products were exported to Mexico in 2022. U.S. petroleum product exports to Mexico increased 33% over 2021. U.S. natural gas exports to Mexico were 4% lower in 2022 than the 2021 average.

On Wall Street for the month of June, the Dow Jones Industrial Average gained 4.6%, the S&P 500 Index rose 6.5% and the Nasdaq Composite gained 6.6%.

Source: Institute for Supply Management Manufacturing Report

on Business and U.S. Census Bureau

For the second quarter, The Dow Jones Industrial Average advanced 3.4%, the S&P 500 Index rose 8.3% and the Nasdaq Composite gained 12.8%. The Nasdaq Composite had its best first half since 1983, surging 31.7%. Recent economic data reinforced investors’ belief that the economy remains resilient and inflation will continue to come down.

Reference

The S&P Return figures are provided by Capital IQ.