The Indian Water and Wastewater Industry

While major global economies are still feeling the effects of the 2009 recession, signs of strength are occurring in the Indian economy. Investor confidence

has largely been restored, and investments that had been suspended due to the slowdown in demand are beginning to pick up pace.

Water has become a crucial commodity in many regions, India not excluded. Emphasis on water quality, coupled with stringent wastewater discharge regulations, are creating

opportunities for the water and wastewater space to see the potential for significant growth. This creates an opportunistic scenario for pumps suppliers.

Reasons for Pump Market Growth

India has been a traditional producer of pumps with a sevendecade history. However, it is only with the recent globalization that the country is marking and increasing its presence in the world pump market. India produces more than two million pump units per year, with about 95 percent of demand accounted for by domestic manufacturers and

imports making up the remaining percentage.

The water and wastewater sector is one of the top three end-user markets for pumps in India and is expected to be a strong area of demand for pump manufacturers through the next decade.

Several key factors are driving opportunity and growth in the Indian water and wastewater industry, as well as the pump industry as a whole:

• Maintaining and enhancing water quality—increased regulations, efficient legislation and pragmatic guidelines are expected to be areas of focus. This is important if environmental degradation is to be eventually controlled and reversed. Compliance will become an important measure for the industry.

• Infrastructure expansion—India's gross domestic product (GDP) growth has hovered at about 8 percent, and infrastructure-related development investments in the 11th Five Year Plan are planned in the multiple billions.

• Challenges in water management, created by several factors:

1. India's growing economy, increasing middle class, expanding infrastructure and vast agricultural region are contributing to water challenges. India is the world's largest user of groundwater, using about 230 cubic kilometers every year (more than one quarter of the global total). With the prevalent drought conditions in many arid states due to inadequate rainfall, groundwater levels have been depleting at a rapid pace. This is expected to increase demand for pressure booster and deep well submersible pumps to draw water from greater depths.

2. Urbanization of the country has lead to the migration of more than one billion people from villages to major cities, creating pressure on the existing infrastructure, including the delivery of utility water after removal and treatment of wastewater.

3. Rising consumption and decreasing supply of uncontaminated water is driving the growth of desalination plants in this country, also a boon for pumps.

India's emergence as a low-cost manufacturing hub—India has a dual advantage of low-cost labor and highly technical, skilled manpower. This is an enticing proposition to the western multinational pump manufacturers that can set up manufacturing facilities and reduce production costs by substantial levels. This scenario facilitates not only addressing the increasing domestic demand but also in exporting pumps to neighboring regions, including the Asian growth engine countries.

Growing real estate/housing sector—growth in this specific portion of infrastructure is expected to increase demand for energy efficient water pumps, offering both cost savings and reduction of carbon footprint.

Market Challenges

While this market holds great promise for increasing pump revenues in the water and wastewater space, many factors challenge sustained market growth. One is the continued potential for political instability, which can have significant negative effects on projects funded by the government. A change in government tends to delay or abolish planned projects, particularly in the water and wastewater sector.

A further issue is the inconsistency in the implementation of environmental standards at the state level. This is a major restraint on market growth in that most states do not have systems in place to monitor water pollution levels sufficiently, systematically and consistently. Moreover, environmental agencies have not been granted firm support or influential legislative mandates, limiting their capacity to be effective. A lack of conscious efforts for the enforcement of environmental legislation can affect the growth in the pumps market.

Projected Growth

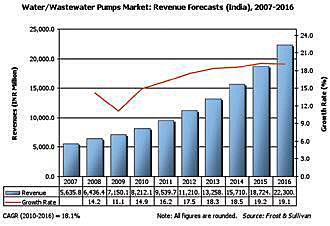

Figure 1. Forecast for the Indian water and wastewater pump industry through 2016.

In spite of these issues, the overall Indian pumps market in the water and wastewater sector is expected to continue in growth mode. Figure 1 shows Frost & Sullivan's forecast for this industry through 2016.

In Figure 1, revenues in the base year of 2010 were an estimated 5,635.8 million Indian rupees (INR), which translates, based on January 2011 conversion rates, to just under $124 million (which includes both centrifugal and positive displacement [PD] pumps). Currently, centrifugal is the bulk of this number, constituting approximately over 95 percent of revenues. While growth is expected for both types of pumps, centrifugal units are expected to continue to be heavily favoredin demand. The compound annual growth rate for pumps in this sector is forecast at just over 18 percent, based on the growth trends indicated for the country as well as the industry.

Centrifugal pumps play a pivotal role in municipal water supply and irrigation projects. With many projects lined up in both these areas during the forecast period, strong growth is projected for these units. PD pumps are largely confined to wastewater treatment and sanitary requirements. Lack of awareness among end users and consultants about the energy savings potential from these units is a deterrent for growth in this type pump.

Overall, rising water demand in India due to increasing population and rapid urbanization is expected to drive a variety of infrastructure activities, from industrial/commercial/ municipal water treatment and distribution to wastewater applications to desalination projects. Additionally, increased regulations and more strict compliance enforcement point to a robust scenario for the water and wastewater sector in India over the next decade.

Pumps & Systems, March 2011