Pumps What’s Next: 2025 State of the Industry Outlook Economist Chris Angle and pump industry expert Tom Angle provide a look at the road ahead.

Pump Industry Insider Economic Outlook: December 2024 The United States Bureau of Labor Statistics reported the Consumer Price Index for All Urban Consumers (CPI-U) rose by 0.2% in September.

Pump Industry Insider Economic Outlook: November 2024 In August, U.S. import prices dropped by 0.3%, the largest decline since December 2023.

Economic Outlook: October 2024 In July, U.S. import prices increased by 0.1%, following no change in June, driven by rises in both fuel and nonfuel import prices.

Economic Outlook: September 2024 The Producer Price Index (PPI) for final demand rose 0.2% in June, following no change in May and a 0.5% increase in April.

Pump Industry Insider Economic Outlook: August 2024 U.S. import prices fell by 0.4%, following a 0.9% increase in April, driven by decreases in both fuel and nonfuel import prices.

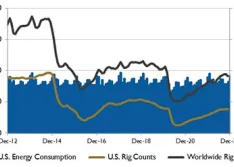

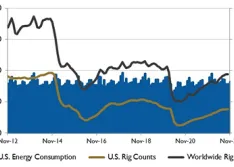

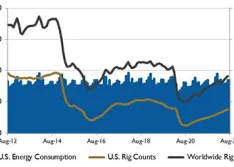

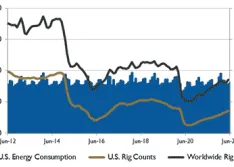

Pump Industry Insider Wall Street Pump & Valve Industry Watch, December 2023 Production cuts are expected to keep global oil production below global oil consumption next year.

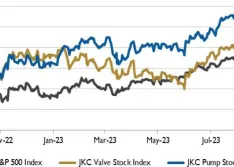

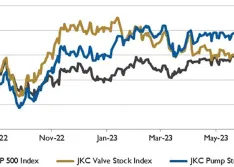

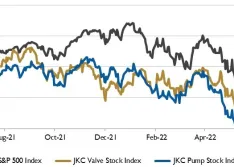

Pump Industry Insider Wall Street Pump & Valve Industry Watch, September 2023 JKC pump stock index, payrolls & unemployment rates increase.

Pump Industry Insider Wall Street Pump & Valve Industry Watch, August 2023 The Customers’ Inventories Index dropped into “too low” territory (46.2% versus 51.4%), a positive sign for future production.

Pump Industry Insider Wall Street Pump & Valve Industry Watch, May 2023 The employment index fell for the third straight month to 46.9%, its lowest reading since 2020.

Pump Industry Insider Wall Street Pump & Valve Industry Watch, April 2023 Markets were volatile due to fears of continued interest rate hikes.

Pump Industry Insider Wall Street Pump & Valve Industry Watch, March 2023 The S&P 500 posted its best January since 2019.

Pump Industry Insider Wall Street Pump & Valve Industry Watch, February 2023 The markets finished the year with their worst results since 2008.

Pump Industry Insider Wall Street Pump & Valve Industry Watch, January 2023 Any unplanned supply disruption has the potential to increase oil prices quickly and significantly.

Pumps Wall Street Pump & Valve Industry Watch, December 2022 Exploration activity has been up and down this year.

Pumps Wall Street Pump & Valve Industry Watch, November 2022 The employment index fell back into contraction territory.

Pumps Wall Street Pump & Valve Industry Watch, October 2022 Amid concerns about slower growth for the global economy, the Export Orders Index slipped into contraction territory.

Pumps Wall Street Pump & Valve Industry Watch, September 2022 Government spending declined for a third straight quarter.

Pumps Wall Street Pump & Valve Industry Watch, August 2022 Major stock indexes have fallen in the last year.

Pumps Wall Street Pump & Valve Industry Watch, July 2022 Customer inventories had its largest decline in six months.

Extend Your Pump's Lifespan With Greene Tweed's High-Performance WR Materials Enhance performance and durability in extreme conditions with advanced, reliable solutions. Sponsored byGreene Tweed

Redefining Pump Performance: Long Runs, Simple Installs & More Power With Clean Power VFD Learn how SmartD’s Clean Power VFD fundamentally simplifies long cable installations and much more in this webinar. Sponsored bySmartD Technologies

Best Practices in Pump Piping Systems Gain a thorough understanding of piping applications for pumped systems, with special focus on suction and discharge piping requirements. Sponsored byVaughan Co, Inc.

Road Map to 5 Years MTBF for Hot Oil Pumps Discover essential strategies to attaining 5-year mean time between failure on industrial hot oil pumps. Sponsored byKlaus Union

The Benefits of AODD Pumps in Explosive Environments Learn about examples of AODD pumps in explosive applications, how to select an explosion-proof AODD pump and much more in this webinar. Sponsored byWilden